foreword

Can transformative innovations become our climate saviour?

IKE Institute CEO Professor Sa’ad Sam Medhat explores how disruptive innovation can help in the fight against climate change, the areas where it is most needed, and the potential positive impact of responsible innovation.

Disruptive innovations continue to enable numerous responses to the Covid-19 pandemic. Technologies adopted include online health care; blockchain-based epidemic monitoring platforms; robots that deliver food and medications and screen people’s temperatures; online education platforms and home-based working solutions; as well as robotics and 3D-print technologies to manage safe working environments in manufacturing plants.

So, could this trend of globally concerted innovations provide a similar impetus for capacity-building climate change innovations and, thus, support the realisation of the United Nation’s 17 Sustainable Development Goals (SDGs) by 2030?

Within the UN’s SDGs, innovation is explicitly referenced in SDG 9 – Industry, Innovation and Infrastructure. The indicators used to monitor innovation within SDGs measure the R&D spend per capita and the number of researchers in R&D per million population.

At the IKE Institute, we believe this measure of innovation within the SDGs that is solely linked to R&D reflects a narrow view of innovation. We argue that using a broader definition of innovation is critical to achieving all the SDGs as well as ‘making peace with nature’.

Defining innovation in a climate change context

Public and private spending on R&D related to climate change adaptation as a share of GDP remains limited and concentrated in a few countries, according to a recent report by the World Bank. It highlights that the number of patented inventions in technologies for climate change adaptation globally has increased steadily over the last two decades.

The report also points out that cross-border technology transfers of innovation to adapt to climate change is concentrated within a limited number of countries. China, Germany, Japan, the Republic of Korea, and the United States together account for nearly two thirds of all high-value inventions (technological inventions seeking patents in more than one country) filed globally between 2010 and 2015.

The OECD’s Oslo Manual on the Measurement of Innovation defines innovation as ‘a new or improved product or process (or combination thereof) that differs significantly from the unit’s previous products or processes, and that has been made available to potential users (product) or brought into use by the unit (process)’.

The OECD Oslo indicators for measuring innovation have a greater focus on innovation by adoption, including augmentation of processes, enhancements of existing products, services, techniques and business models, smarter and productive working practices, with a key indicator being growth in jobs and the quality of those jobs.

Meeting SDGs through the adoption of frontier technologies

If one examines these two views of innovation given by the UN and OECD respectively, a certain contradiction in interpretation can be seen, in that the former determines innovation by invention, and the later sees innovation by adoption.

Business adoption of innovation, either new technologies or new approaches, is driven by the expectation of future profits. It depends on the availability of necessary capital and a willing and capable workforce.

These concepts are often referred to as the ‘adaptive capacity’ within a business. Analysis suggests a growing workforce, with good qualifications, is an important factor. And today, the ‘frontier’ technologies and approaches are usually geared towards tertiary qualified individuals.

Investment in such new technologies, processes and products have multiple benefits in helping to meet some of the SDGs including:

- SDG 3: Good Health and Well-Being – Reduction of Polluting Emissions;

- SDG 8: Decent Work and Economic Growth – Productivity Gains;

- SDG 9: Industry, Innovation and Infrastructure – Efficiency Gains;

- SDG 12: Responsible Consumption and Production;

- SDG 13: Climate Action – Carbon Intensity Reductions.

A critical driver of acceptance of frontier technologies is the entry cost barrier, which is often driven down by increasing market size. Usually, technical improvements can be adopted quicker in an expanding market, mainly through investment in new capital plants that make the products.

Government support in various forms for adoption of frontier technologies can help to grow the market size and reduce costs. In the past, public interventions have taken many forms, including support for basic and developmental research, grants, feed-in-tariffs and other subsidies. These have been proven to work in such areas as low-carbon reductions and renewable technologies (Gillingham K, Stock JH, 2018).

Grand challenges for innovation

Grand challenges and remaining missions, similar to those that produced the cost reductions of renewable electricity, now need to be applied to other fields, including the following:

- Financial innovation for zero-carbon world

- Negative carbon and carbon offsets

- Adaptation to the consequences of climate change

- Green hydrogen

- Agriculture and food systems

- Protecting natural capital

- Blue carbon

Financial innovation for a zero-carbon world

Adoption of renewables needs to speed up, especially in Africa, and this will only happen if changes are quickly made to how the financial system operates. Similarly, existing capital plants for power generation and manufacturing will need to be written-off and replaced to allow them to become more efficient and sustainable.

Achieving this without collapsing the economy requires careful and innovative financial management. As Mark Carney puts it in his book Value(s): Building a better world for all: “With comprehensive climate disclosure, a transformation in climate risk management and by the mainstreaming of sustainable investment, we can ensure that every financial decision takes climate change into account.”

Negative carbon and carbon offsets

According to Our World in Data analysis, the carbon dioxide (CO₂) intensity of economies measured in kilograms of CO₂ per $ of GDP (measured in international dollars in 2011 prices) demonstrates that most countries need to reduce the carbon intensity of their economies, which will require the replacement of current industrial plants and practices. Given this, some oil producing countries will be particularly challenged.

Most plans for net zero by companies and countries involve the use of negative carbon, or carbon offsets based on carbon sequestration. Some carbon offset schemes are controversial and there are no international, externally verified and monitored standards for offsetting.

There are some verified reforestation schemes, but there are few verified schemes outside of reforestation. Even with re-forestation, schemes often operate alongside effective subsidies for de-forestation elsewhere. Although there has been some reforestation of temperate forests, this does not replace historic temperate deforestation. Deforestation of tropical forests peaked in the 1980s but there is still plenty of scope for stopping deforestation and encouraging tropical reforestation.

Carbon offsets should not be an excuse by companies or governments for avoiding achievable carbon reductions. With renewables now often cheaper than fossil fuelled plants, the efforts should now be on closing fossil fuelled plants rather than subsidising renewables.

Adaptation to the consequences of climate change

There is a growing list of climate-driven consequences of growing intensity, ranging from rising sea levels, erratic and extreme weather, droughts, excessive heat, fires, and humidity, to storms and flooding. Greater levels of adaptation are unquestionably required, as a significant proportion of global assets are at threat from these consequences of climate change.

Many of the existing responses to adaptation requirements involve unsustainable amounts of concrete and high costs, as a Chatham House report titled ‘Making concrete change’ from 2018 highlights. Innovation, and more importantly, transformative innovation is urgently required to combat the dramatic climate change challenge.

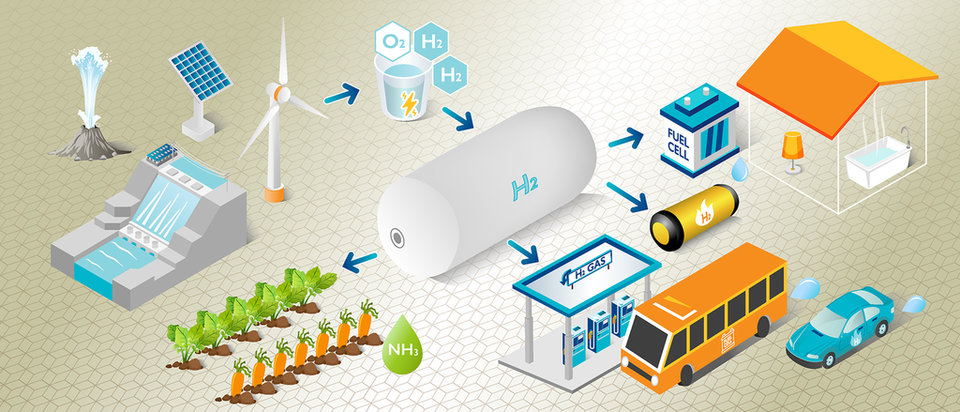

Green hydrogen

The UK’s new hydrogen strategy, announced in August 2021, sets out the approach to developing a thriving low carbon hydrogen sector in the UK to meet the government’s ambition for 5GW of low carbon hydrogen production capacity by 2030.

The production and use of green hydrogen for process heat, shipping and heavy vehicles is needed. It also produces ammonia, the starting point for nitrogen fertilizers. Scientists are actively developing hydrolysis catalysts, direct hydrogen production from sunlight and putty/gel storage systems. The need is for support mechanisms to fund, deploy and improve cost effectiveness of these processes.

It is also worth pointing out that the cost of fuel cell electric vehicles versus battery electric vehicles is becoming comparable and is likely to reduce in the future.

According to a report published by the Hydrogen Council in January 2020, significant cost reductions are expected across different hydrogen applications, in areas such as long-distance and heavy-duty transportation, industrial heating, and heavy industry feedstock, all of which roughly make up 15% of global energy consumption, thus positioning the hydrogen route as the decarbonisation option of choice.

To deliver on this opportunity, supporting policies will be required in key geographies, together with investment support of around $70bn in the lead up to 2030, in order to scale up and achieve hydrogen competitiveness. Whilst this figure might look sizable, it accounts for less than 5% of annual global spending on energy.

Illustration of the value chain for green hydrogen

Agriculture and food systems

A recent study published in Nature calculates that a third of global greenhouse gas emissions (CO₂, CH4, N20 and fluorinated gases) are associated with food systems.

Based on the EDGAR-FOOD database, food systems account for 18gT CO₂ equivalent per year, or 34% of total emissions, of which, in 2015, agriculture represented 32%, with land-use and land-use change a further 39%. The remaining 29% result from supply chain activities, retail, transport, consumption, fuel production, waste management, industrial processes, and packaging.

Protecting natural capital

Aside from being a major cause of emissions, our current food system has a huge impact on land use and biodiversity. Protecting natural capital is a key aspect of creating sustainability in food production.

“Today, we ourselves, together with the livestock we rear for food, constitute 96% of the mass of all mammals on the planet,” David Attenborough said in 2021. “Only 4% is everything else – from elephants to badgers, from moose to monkeys. And 70% of all birds alive at this moment are poultry – mostly chickens for us to eat.”

Yet, biodiversity is a key component of natural capital, which provides massive ecosystem services such as flood protection, sequestration of CO₂ and nitrates, and improved air quality. There is, of course, a need to balance the demands of meeting SDG 2: Zero Hunger with the need to meet SDG 13: Climate Action, SDG 14: Life Below Water and SDG 15: Life on Land.

Blue carbon

Carbon sequestration in the inter-tidal areas and offshore has great potential. This requires changes to fishing practices and usage of inter-tidal areas.

Rehabilitation of these sorts of areas can sequester up to five times the carbon as rehabilitating tropical forests. There are research requirements to understand the types of fishing and aquaculture practices that are consistent with saving blue carbon. (More information on this can be found in the Blue Carbon Initiative’s manual ‘Coastal blue carbon: methods for assessing carbon stocks and emissions factors in mangroves, tidal salt marshes, and seagrass meadows’.)

This rehabilitation effort has important implications for meeting SDG 14 – Life Below Water.

Other areas requiring innovation

We have identified three other areas related to climate change that require specific innovation attention. These are:

- Dealing with the CO₂ emissions inherent in the current cement and steel making processes.

- Aviation, although only contributing 1% of global emissions, is symbolic and needs to find ways to be zero-carbon.

- Heating and cooling dwellings uses an increasing amount of energy, and therefore, greater efficiencies are required.

Responsible innovation leaders

The setting of enforceable emission limits linked to a price on carbon pollution is an essential component of any successful long-term strategy to meet our climate goals. At the same time, it is important to increase our commitment to the research and development needed to bring to market the next generation of innovative low and zero carbon technologies.

Responsible innovation (RI) has been formally defined as “careful consideration of, and action to address, the potential impacts of introducing a new product, service, process or business model must consider the benefits that are derived from innovation and seeks to eliminate, minimise or mitigate any potential downsides from the perspectives of the company, its employees, suppliers and customers and stakeholders”, according to the BSI’s publicly available specification document PAS 440:2020 Responsible Innovation - Guide.

We at the IKE Institute describe responsible innovation as the result of three main intersecting contexts. The governance context, which includes the rules, regulations and policies within which RI occurs. The innovation context, which includes the technical possibilities and the social responsibility priorities set by governments including the UN SDGs. And the stakeholder engagement context, which needs to include the whole business, and this requires transparency about the direction of its innovation and the likely outcomes.

Responsible innovation focuses on the role of an organisation in addressing grand global and societal challenges and see innovation as transformative.

Therefore, responsible innovation focuses on the role of an organisation in addressing grand global and societal challenges and see innovation as transformative. Responsible innovation presents a critical role for government in de-risking innovation and recognising the importance of the precautionary principle. Responsible innovation demands responsible leadership to co-ordinate all the aforementioned intersecting contexts and pressures.

If a long-term governmental strategy is to be successful in meeting climate action goals, it must have components focused on enforceable reduction in emissions linked to the price on carbon pollution. However, at the same time, it is important to generate collective action that brings together responsible leaders from the public and private sector, including government officials, scientists, entrepreneurs, and financiers.

Such collective action is essential in increasing commitment to delivering the R&D needed to bring to market the next generation of innovative low and zero carbon technologies at pace and scale, to support the creation of viable solutions and changes in behaviour.

Such connected and escalated pathways, similar to those exerted by the Covid-19 intensified R&D efforts, can bring together the transformative value creation needed for radical progress in climate change innovations, adaptations, and ultimately, achieve the bottom line: our planet’s survival.

Professor Sa’ad Sam Medhat

PhD MPhil CEng FIET FCIM FCMI FRSA FIKE FIoD

Chief Executive

Institute of Innovation and Knowledge Exchange

Share this article